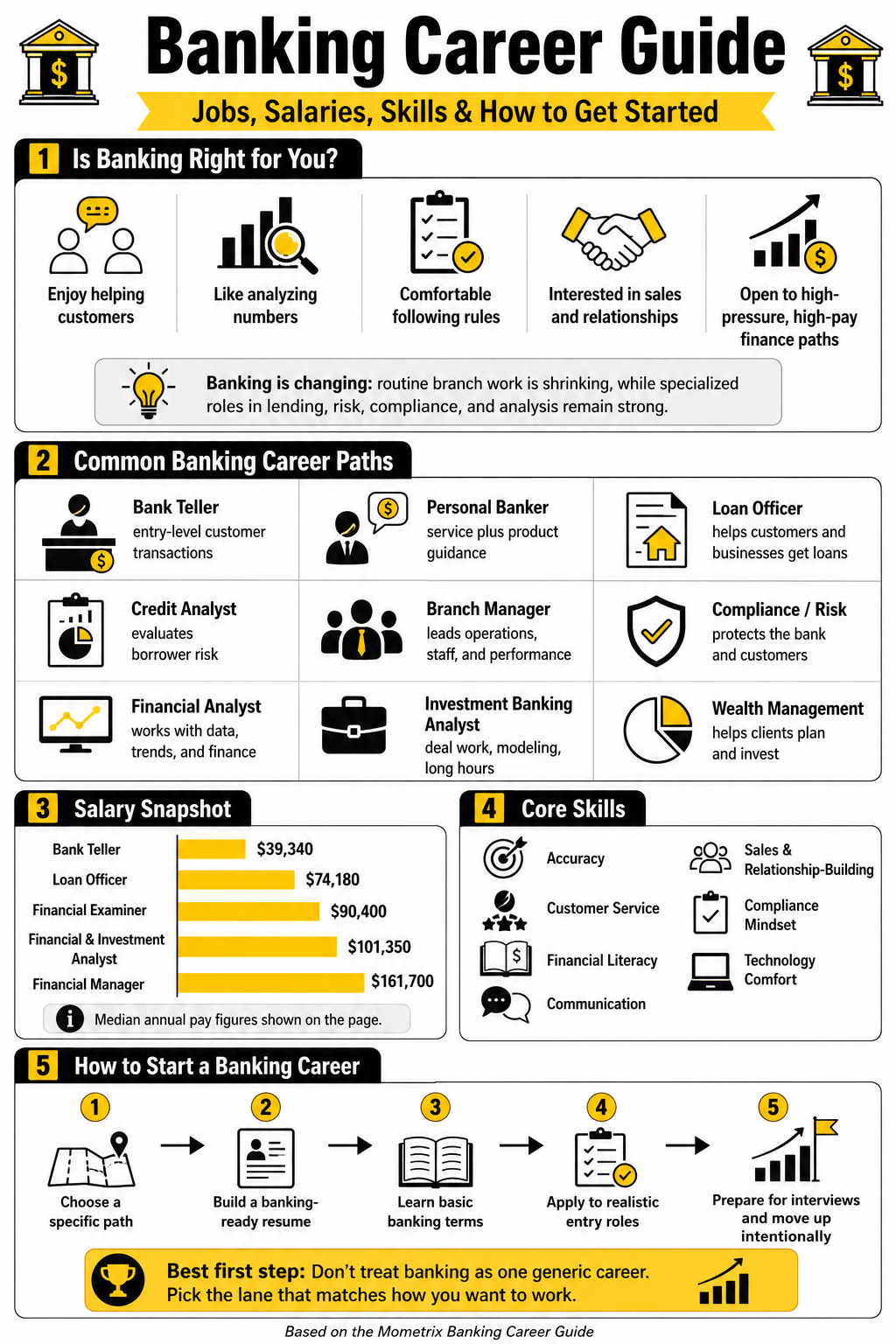

A banking career can be a strong fit if you like working with numbers, helping people make financial decisions, following clear rules, and building trust. But “banking” is not one career. It includes branch banking, lending, credit analysis, compliance, risk management, operations, wealth management, financial analysis, and investment banking.

That matters because each path has a different lifestyle, education requirement, salary range, and long-term upside.

Some banking careers are customer-facing. Some are analytical. Some are sales-heavy. Some are compliance-driven. The best banking career path for you depends on how you want to spend your workday.

Is Banking a Good Career Path?

Banking can be a good career path if you want a business-focused job with clear advancement opportunities. Many people start in entry-level branch, customer service, operations, or lending support roles and move into higher-paying areas such as commercial banking, credit analysis, risk, compliance, financial analysis, wealth management, or management.

Banking is not a perfect fit for everyone. You may struggle in banking if you dislike rules, documentation, accuracy, customer service, sales expectations, or accountability for financial details.

A better way to think about it:

- If you enjoy helping customers directly, consider branch banking or relationship banking.

- If you enjoy analyzing numbers, consider credit analysis, financial analysis, or risk.

- If you enjoy rules and investigation, consider compliance, audit, fraud, or financial examiner roles.

- If you enjoy sales and financial products, consider lending, private banking, or wealth management.

- If you want high pay and can handle long hours and pressure, investment banking may be worth exploring.

Banking is not dying, but it is changing. Routine transaction roles face pressure from online and mobile banking. Specialized roles involving analysis, advice, lending, compliance, risk, fraud prevention, and technology are more resilient.

What Is a Banking Career?

A banking career is any job that helps a financial institution serve customers, manage money, evaluate risk, process transactions, lend funds, protect assets, or follow financial regulations.

Banking employers may include:

- Retail banks

- Credit unions

- Commercial banks

- Investment banks

- Mortgage lenders

- Wealth management firms

- Financial technology companies

- Banking regulators

- Government agencies

Some banking jobs require only a high school diploma or equivalent. Others usually require a bachelor’s degree in finance, accounting, economics, business, mathematics, statistics, data analytics, or a related field.

Common Banking Career Paths

Bank Teller

Bank tellers process deposits, withdrawals, payments, checks, and other everyday transactions. They also answer basic account questions and help customers with routine banking needs.

Best for: Entry-level candidates, customer service workers, students, and people who want to learn bank operations.

Common requirements: High school diploma or equivalent, basic math, accuracy, cash handling, and customer service skills.

Possible next steps: Senior teller, personal banker, branch supervisor, assistant branch manager, branch manager, operations associate, or fraud support.

Reality check: Teller jobs can be a useful way to enter banking, but they should be treated as a launchpad. Digital banking has reduced demand for routine transaction work.

Personal Banker or Relationship Banker

Personal bankers help customers open accounts, understand banking products, resolve account issues, and connect with services such as credit cards, loans, mortgages, or investment referrals.

Best for: People who like customer conversations, problem-solving, and ethical sales.

Common requirements: High school diploma or equivalent; some employers prefer a bachelor’s degree or prior sales/customer service experience.

Possible next steps: Senior banker, relationship banker, branch manager, business banker, mortgage banker, or wealth management associate.

Reality check: This role often includes sales goals, referral goals, or customer-growth targets. It is not just a service desk job.

Loan Officer

Loan officers help people or businesses apply for loans. They review financial information, explain loan options, collect documents, and guide borrowers through the approval process.

Best for: People who like sales, finance, documentation, and customer guidance.

Common requirements: Requirements vary by loan type. Mortgage loan originators may need licensing. Commercial lending roles often prefer a bachelor’s degree.

Possible next steps: Senior loan officer, lending manager, commercial banker, portfolio manager, or credit leadership.

Reality check: Loan officer income can vary with market conditions, interest rates, loan volume, and commission structure.

Credit Analyst

Credit analysts review financial statements, cash flow, credit history, collateral, and repayment risk. Their work helps banks decide whether to approve loans and under what terms.

Best for: Analytical thinkers who like spreadsheets, financial statements, and risk evaluation.

Common requirements: Bachelor’s degree in finance, accounting, economics, business, or a related field. Excel and financial statement analysis are important.

Possible next steps: Senior credit analyst, portfolio manager, commercial lender, credit officer, risk analyst, or underwriting manager.

Reality check: Credit analysis is one of the strongest entry points for people who want a serious long-term banking career without starting in a branch.

Branch Manager

Branch managers oversee employees, customer service, operations, sales performance, compliance, and local business development for a bank branch.

Best for: People who can lead teams, coach employees, manage customer issues, and hit business goals.

Common requirements: Several years of banking, sales, or retail management experience. A degree may help, but it is not always mandatory.

Possible next steps: District manager, regional manager, retail banking leadership, business banking, or operations leadership.

Reality check: Branch management is a leadership role. You are accountable for people, performance, customer experience, risk, and operations.

Compliance, Risk, Audit, and Fraud Roles

Banks operate under strict rules. Compliance officers, risk analysts, internal auditors, fraud analysts, and financial crime specialists help banks prevent losses, protect customers, and follow regulations.

Best for: Detail-oriented people who like rules, investigation, documentation, and risk prevention.

Common requirements: Bachelor’s degree is often preferred. Relevant coursework in finance, accounting, law, criminal justice, data analytics, or business can help.

Possible next steps: Senior analyst, compliance manager, risk manager, audit manager, fraud investigations manager, or chief compliance/risk officer.

Reality check: These roles are not always visible to customers, but they are extremely important. They can also be more stable than sales-heavy roles.

Financial Analyst

Financial analysts study data, company performance, investments, budgets, markets, or business trends. In banking, they may work in corporate finance, commercial banking, investment analysis, risk, treasury, or planning.

Best for: People who like Excel, financial modeling, data, research, and business decision-making.

Common requirements: Bachelor’s degree in finance, accounting, economics, business, mathematics, statistics, or a related field.

Possible next steps: Senior financial analyst, finance manager, investment analyst, portfolio analyst, corporate finance, or strategy roles.

Reality check: This is a stronger fit for people who want analytical work than for people who primarily want customer interaction.

Investment Banking Analyst

Investment banking analysts work on transactions such as mergers, acquisitions, debt offerings, equity offerings, valuation, and financial modeling.

Best for: High-performing students or early-career professionals who want finance-intensive work and can tolerate long hours.

Common requirements: Bachelor’s degree, strong finance/accounting knowledge, Excel and modeling ability, internships, and a competitive recruiting profile.

Possible next steps: Associate, vice president, private equity, corporate development, venture capital, hedge funds, or business school.

Reality check: Investment banking is not the same as general banking. It can pay well, but the hours and pressure can be intense.

Wealth Management or Financial Advisor

Wealth management professionals help clients plan investments, retirement, estate goals, tax strategies, and broader financial decisions.

Best for: People who like personal finance, investing, relationship-building, and long-term client service.

Common requirements: A bachelor’s degree may be preferred. Securities licenses or advisory credentials may be required depending on the role.

Possible next steps: Financial advisor, senior advisor, wealth manager, private banker, or portfolio advisor.

Reality check: Early years may involve sales, networking, and building a client base. Technical knowledge alone is not enough.

Banking Career Salary Snapshot

Pay varies by role, employer, city, experience, incentives, and performance. Use national medians as a baseline, not a promise.

Role: Bank Teller

Useful starting point: High school diploma or equivalent

2024 median pay / pay context: $39,340

Outlook context: Projected decline

Role: Loan Officer

Useful starting point: Lending support, sales, finance coursework

2024 median pay / pay context: $74,180

Outlook context: Cyclical and market-sensitive

Role: Financial and Investment Analyst

Useful starting point: Finance, accounting, or economics degree

2024 median pay / pay context: $101,350

Outlook context: Strong analytical path

Role: Financial Examiner

Useful starting point: Finance, accounting, or business degree

2024 median pay / pay context: $90,400

Outlook context: Strong compliance/risk path

Role: Financial Manager

Useful starting point: Degree plus experience

2024 median pay / pay context: $161,700

Outlook context: Senior-level goal, not entry-level

Do not choose a banking career based only on the highest salary number. The better question is: which path fits your skills well enough that you can advance?

Skills You Need for a Banking Career

Accuracy

Banking involves money, documents, customer information, deadlines, and legal requirements. Accuracy is non-negotiable.

Customer Service

Even analytical banking roles require communication. Customer-facing roles require patience, clarity, and professionalism.

Financial Literacy

You should understand accounts, interest, credit, loans, fees, balances, and basic financial documents.

Communication

Banking employees must explain financial topics clearly. This includes products, risks, fees, application steps, and account issues.

Sales and Relationship-Building

Many banking roles involve recommending products, building trust, and deepening customer relationships.

Compliance Mindset

Banks are heavily regulated. You need to be comfortable following policies and documenting your work.

Technology Comfort

Modern banking relies on digital tools, spreadsheets, customer databases, fraud systems, online platforms, and data analysis.

Education Requirements for Banking Jobs

You can start some banking jobs without a college degree. Teller, customer service, call center, operations, and some branch roles may be open to candidates with a high school diploma or equivalent.

A bachelor’s degree becomes more important for roles in:

- Credit analysis

- Commercial banking

- Financial analysis

- Risk management

- Compliance

- Investment banking

- Wealth management

- Corporate finance

- Banking leadership

- Helpful majors include:

- Finance

- Accounting

- Economics

- Business administration

- Data analytics

- Mathematics

- Statistics

- Computer science

- Information systems

Useful courses include accounting, corporate finance, statistics, business law, economics, Excel, communication, and ethics.

Certifications and Licenses That Can Help

Do not collect credentials randomly. Choose certifications based on the banking path you want.

Potentially useful options include:

- NMLS licensing for mortgage loan originators (NMLS Review Course)

- FINRA licenses for securities-related roles

- Certified Financial Planner, or CFP, for financial planning (CFP Review Course)

- Chartered Financial Analyst, or CFA, for investment analysis and asset management

- Certified Regulatory Compliance Manager, or CRCM, for bank compliance

- Certified Anti-Money Laundering Specialist, or CAMS, for AML and financial crime roles

- CPA for accounting, audit, and finance leadership

Certifications are strongest when paired with relevant experience.

How to Start a Banking Career

1. Choose a specific path

Do not apply to every banking job with the same resume. Decide whether you are targeting branch banking, lending, credit, compliance, operations, wealth management, or investment banking.

2. Build a banking-ready resume

- Highlight experience with:

- Cash handling

- Customer service

- Sales

- Data entry accuracy

- Excel

- Financial coursework

- Confidential information

- Problem-solving

- Compliance or policy work

- Leadership

- Retail, call center, bookkeeping, insurance, real estate, hospitality, office administration, and sales experience can all transfer into banking.

3. Learn basic banking terms

Know the basics before interviews:

- Checking account

- Savings account

- Interest rate

- APR

- Credit score

- Debt-to-income ratio

- Collateral

- Underwriting

- FDIC insurance

- Compliance

- Fraud prevention

- Know Your Customer, or KYC

- Anti-money laundering, or AML

4. Apply to realistic entry points

- Good starting roles include:

- Bank teller

- Customer service representative

- Personal banker

- Loan processor

- Lending assistant

- Operations associate

- Credit analyst trainee

- Compliance analyst

- Financial analyst internship

5. Prepare for behavioral interviews

- Banking interviews often test judgment, accuracy, professionalism, and trustworthiness. Prepare examples of times you:

- Helped an upset customer

- Caught a mistake

- Followed a rule carefully

- Protected confidential information

- Met a goal

- Explained something complicated

- Worked under pressure

6. Move up intentionally

After you land your first banking role, do not drift. Ask what skills, metrics, training, or certifications are needed for the next step. If your employer offers tuition reimbursement or internal training, use it.

Pros and Cons of a Banking Career

Pros

- Many entry-level options

- Clear advancement paths

- Transferable business skills

- Stable demand for specialized financial roles

- Benefits and training at many banks

- Strong pay potential in specialized paths

- Opportunities in lending, compliance, risk, analytics, technology, and wealth management

Cons

- Entry-level pay may be modest

- Sales goals can be stressful

- Routine teller work faces automation pressure

- Rules and documentation can feel rigid

- Mistakes can have serious consequences

- Some roles require long hours

- Advancement may require switching teams, banks, or locations

Banking Career FAQ

Do you need a degree to work at a bank?

Not always. Many teller, customer service, operations, and branch roles may be open to candidates with a high school diploma or equivalent. Analyst, lending, risk, investment, and management roles are more likely to require a bachelor’s degree.

What is the easiest banking job to get?

Bank teller, customer service representative, call center banker, and entry-level operations roles are common starting points. “Easy to get” does not mean easy to do. Banks still look for accuracy, trustworthiness, professionalism, and communication skills.

Can you move up from bank teller?

Yes. Teller experience can lead to personal banker, branch supervisor, assistant manager, branch manager, operations, fraud prevention, or lending support roles. The key is to treat the teller role as a stepping stone and build additional skills.

What banking career pays the most?

Senior financial managers, investment banking roles, commercial banking leadership, wealth management, and specialized risk or quantitative roles can pay well. Compensation varies widely by employer, location, experience, performance, and bonus structure.

Is banking stressful?

It can be. Stress may come from customer issues, sales goals, compliance requirements, transaction accuracy, deadlines, market cycles, or long hours. Branch banking, loan production, compliance, and investment banking each have different types of stress.

Is banking a good career without a degree?

It can be, especially in branch banking, operations, customer service, and some lending support roles. However, a degree or specialized credential can help you move into higher-paying paths such as credit analysis, financial analysis, compliance, risk, and management.

Is investment banking the same as working at a bank?

No. Investment banking is a specialized finance career focused on transactions, valuation, capital raising, and advisory work. It usually has higher pay potential and much longer hours than many retail or commercial banking jobs.